Europe is entering a new phase of aviation decarbonisation.

For decades, aviation depended almost entirely on fossil kerosene. The sector became one of the hardest parts of the economy to decarbonise because aircraft require extremely energy-dense liquid fuels that are safe, stable and globally compatible.

Unlike passenger vehicles, aviation cannot easily electrify at large scale.

Aircraft need molecules.

This is why Sustainable Aviation Fuel has become strategically important.

SAF allows the aviation sector to reduce lifecycle emissions while continuing to use existing aircraft, airports, pipelines and fuel logistics infrastructure. Instead of replacing the aviation system entirely, SAF enables gradual transition using compatible renewable fuels.

This approach is practical.

But it also creates a major challenge.

The scale of aviation fuel demand is enormous.

Europe consumes tens of millions of tonnes of aviation fuel every year. As SAF mandates increase over time, the volume of renewable fuel required will become extremely large. This creates pressure on feedstock supply chains across the entire energy and industrial system.

At present, much of the SAF discussion focuses on lipid-based pathways such as used cooking oil, waste fats and vegetable oils. These pathways are important and will continue to play a valuable role in SAF development.

But there is a structural limitation.

The volume of waste oils available is finite.

Europe cannot build a long-term SAF strategy around feedstocks that exist only in limited quantities. Even with aggressive collection systems, the available supply of used cooking oil and waste fats remains relatively small compared with total aviation fuel demand.

This is not a criticism of HEFA or lipid pathways.

It is simply a question of scale.

As aviation decarbonisation accelerates, Europe will require additional SAF pathways capable of operating at industrial volume using broader renewable carbon resources.

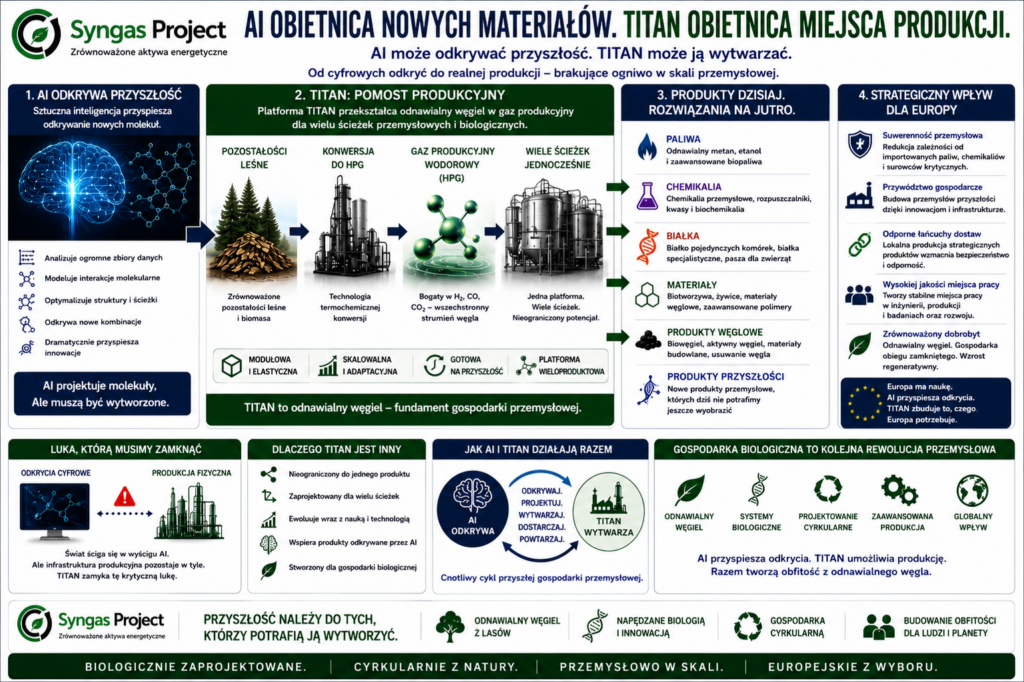

Sztuczna inteligencja zaczyna zmieniać chemię szybciej, niż większość ludzi zdaje sobie z tego sprawę.

Przez dekady odkrywanie nowych materiałów, ścieżek biologicznych i związków przemysłowych było powolne, kosztowne i niepewne. Zespoły badawcze mogły spędzać lata na testowaniu molekuł, enzymów i formulacji z ograniczonym powodzeniem.

To szybko się zmienia.

Sztuczna inteligencja potrafi dziś analizować ogromne ilości danych chemicznych, biologicznych i materiałowych jednocześnie. Może modelować interakcje, optymalizować struktury molekularne i identyfikować zupełnie nowe kombinacje znacznie szybciej niż tradycyjne metody badawcze.

Konsekwencje są ogromne.

AI może pomóc odkrywać:

Nowe paliwa. Nowe tworzywa sztuczne. Nowe białka. Nowe leki. Nowe chemikalia przemysłowe. Nowe materiały biologiczne. Nowe systemy rolnicze. Nowe produkty węglowe.

Rządy i firmy technologiczne inwestują miliardy w tę transformację, ponieważ ci, którzy będą kontrolować następną generację materiałów i molekuł, mogą współtworzyć następną gospodarkę przemysłową.

Ale istnieje problem.

Samo odkrycie nie tworzy przemysłu.

Molekuła odkryta przez sztuczną inteligencję nadal musi zostać wyprodukowana fizycznie, ekonomicznie i w dużej skali.

W tym miejscu rozmowa staje się przemysłowa, a nie cyfrowa.

Świat bardzo szybko buduje systemy sztucznej inteligencji zdolne projektować produkty przyszłości. Jednak fizyczna infrastruktura zdolna do ich produkcji rozwija się znacznie wolniej.

Tworzy to rosnącą lukę pomiędzy cyfrowym odkrywaniem a rzeczywistą produkcją.

Syngas Project uważa, że ta luka może stać się jedną z najważniejszych szans przemysłowych następnego pokolenia.

Ponieważ TITAN nie jest wyłącznie platformą energetyczną.

Jest platformą odnawialnej produkcji węglowej.

Proces TITAN rozpoczyna się od konwersji pozostałości leśnych w Hydrogen Producer Gas (HPG). Tworzy to stabilny gazowy strumień węgla bogaty w wodór, tlenek węgla i dwutlenek węgla. Ten strumień może następnie jednocześnie zasilać wiele ścieżek przemysłowych i biologicznych.

Dziś ścieżki te koncentrują się głównie na produkcji odnawialnego metanu i etanolu.

Jutro te same ścieżki mogą wspierać całkowicie nowe klasy produktów biologicznych i przemysłowych.

Artificial intelligence is rapidly becoming the defining technology race of the 21st century.

Every week brings announcements about larger models, faster processors, more capable software agents and increasingly advanced machine reasoning systems. Governments are investing billions. Technology companies are competing for dominance. Data centres are expanding across the world at extraordinary speed.

Most discussion focuses on computation.

But very little discussion focuses on what artificial intelligence ultimately needs in the physical world.

Because intelligence alone does not manufacture anything.

Artificial intelligence can design molecules. It can optimise biological pathways. It can simulate new materials. It can improve industrial systems. It can accelerate chemistry and biotechnology research.

But eventually, something physical must manufacture the result.

This is where the next industrial bottleneck may emerge.

The future may not belong only to countries that control computation.

It may also belong to countries that control biological manufacturing platforms capable of turning digital intelligence into physical products.

That distinction is becoming increasingly important.

Artificial intelligence is already beginning to transform chemistry, material science, pharmaceutical research, biological engineering and industrial process optimisation. The speed of discovery is accelerating dramatically. New materials, proteins, enzymes, carbon structures and biological production pathways are being identified faster than traditional industrial systems can adapt.

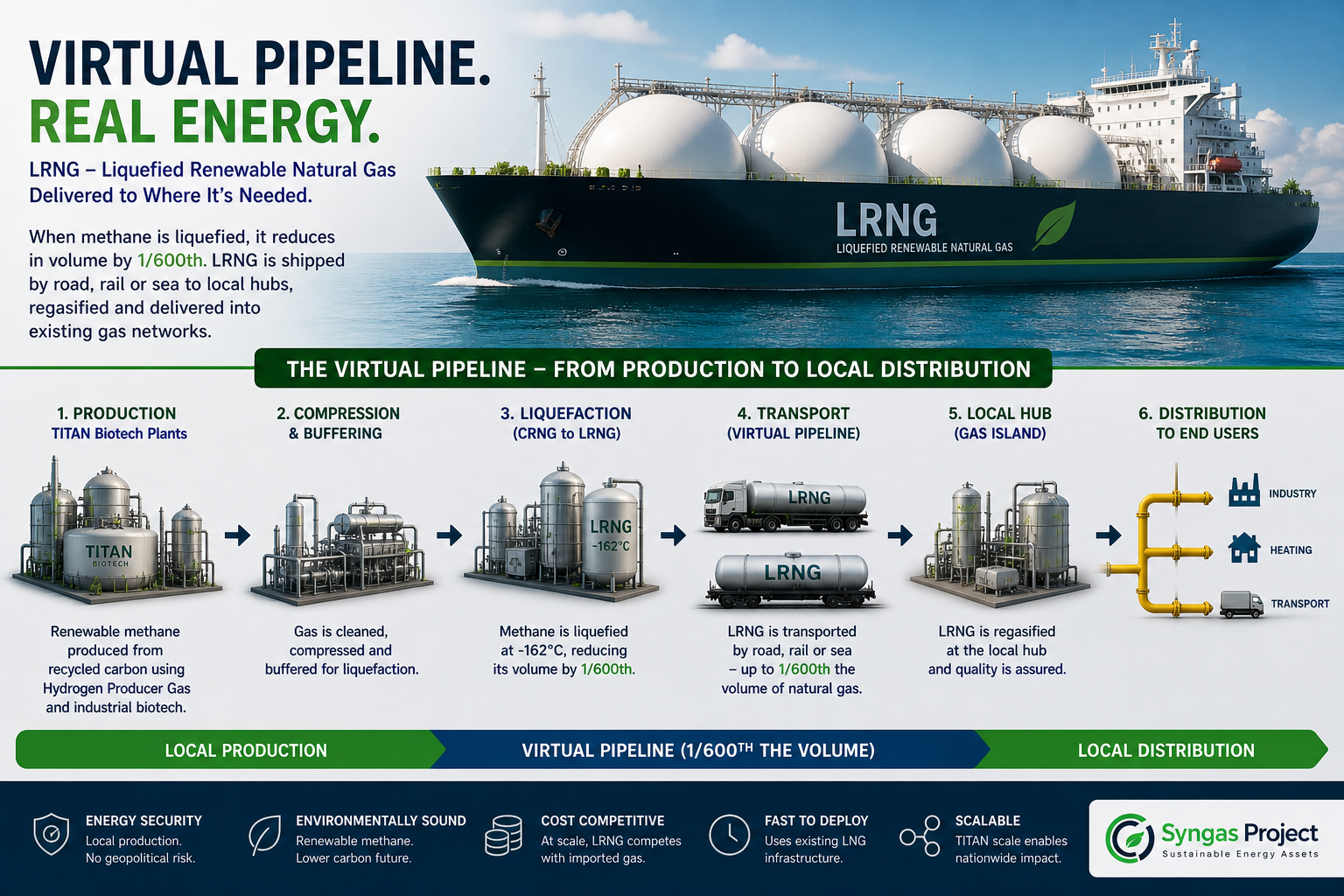

Europe does not have a gas problem. It has a gas origin problem.

Methane remains essential. It fuels industry, supports energy resilience, underpins logistics and provides the backbone for large parts of the economy that cannot simply electrify. The system that distributes methane is already built. What is changing is not the need for gas, but where that gas comes from.

Today, gas is distributed increasingly in liquefied form. LNG has already proven the model. Methane is cooled, liquefied and reduced to around 1/600th of its original volume. It is then transported efficiently by ship, rail or road tanker, delivered to a local hub, regasified and supplied into the network.

This is not a workaround. It is the system.

Many still think LNG distribution is an excuse for not having pipelines. That is wrong. LNG is a more targeted delivery system. The local hub receives the gas it ordered, not a blended molecule that entered a pipeline thousands of kilometres away. The control point moves from the pipeline to the destination.

The real legacy of the gas system is not the intercontinental pipeline.

It is the local gas network.

Historically, gas was produced locally and distributed locally. Towns and industrial centres had their own gas production linked directly to local demand. Long-distance pipelines came much later. They replaced local producers and centralised supply, often for convenience and scale. For a period, that worked.

Today, that model is under pressure.

Russia to the east is no longer a reliable source. Conflict in the Middle East continues to destabilise global energy flows. The United States is becoming less dependable as a long-term strategic partner. Norway carried Europe through the immediate crisis, but it is past peak. It delivered when needed, but production will not keep expanding. The longer global instability continues, the more pressure is placed on a limited northern supply base.

Europe is still climbing an import ladder that is no longer secure.

At some point, that ladder has to be left behind.

Poland has an alternative.

Poland already operates a distributed gas system. The LNG terminal near Szczecin has been built out from approximately 6 billion cubic metres toward 8 billion cubic metres of capacity. More importantly, more than 100 LNG regasification gas islands developed by PSG already form a decentralised distribution network across the country.

These are not temporary assets. They are long-life infrastructure.

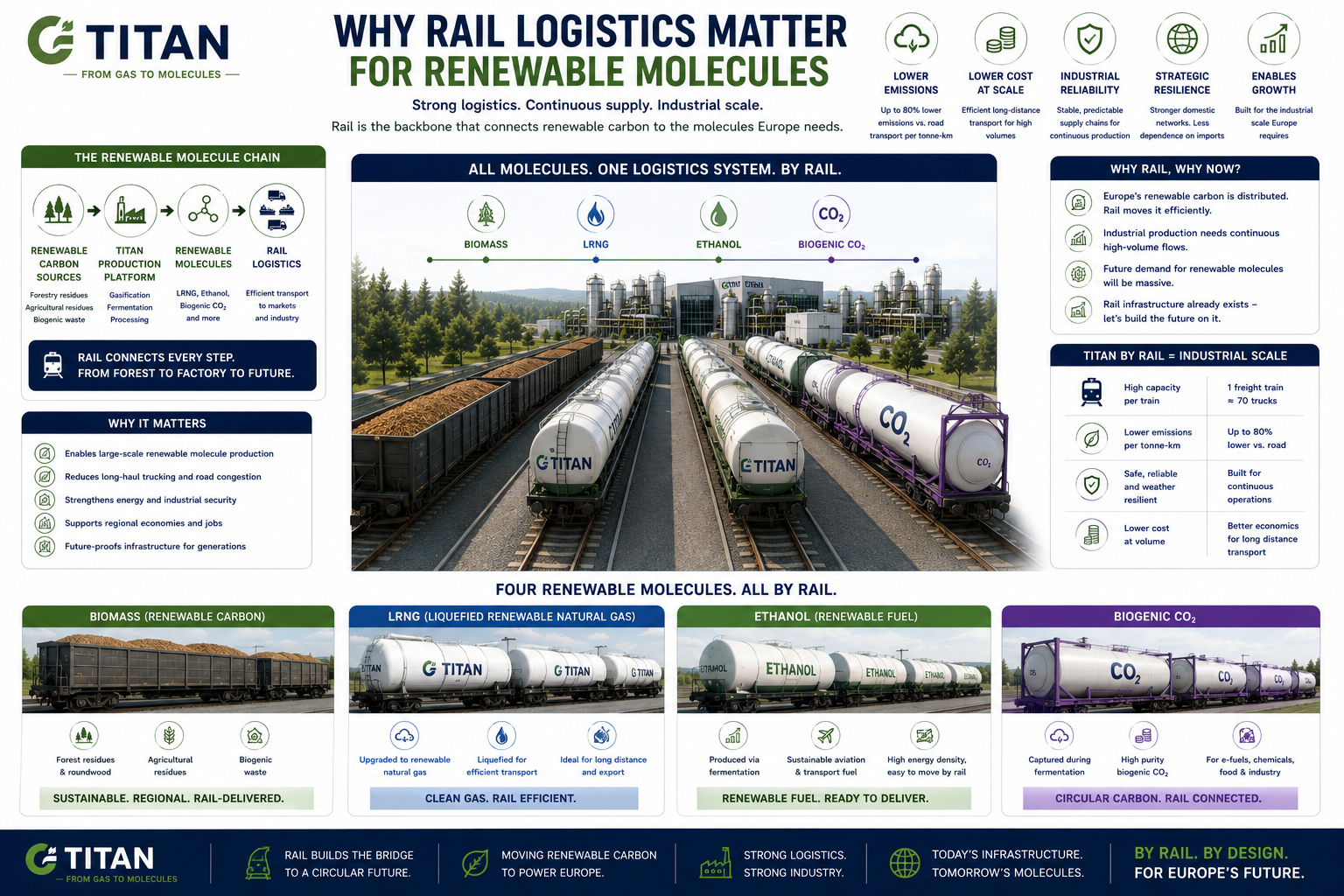

The renewable molecule economy will not succeed on chemistry alone.

It will succeed on logistics.

One of the largest mistakes in modern energy planning is the assumption that low-carbon systems can simply replace fossil systems without rebuilding the underlying industrial transport infrastructure. In reality, renewable molecules require an entirely different logistical approach.

This is especially true at industrial scale.

Renewable carbon is more distributed than fossil carbon. Biomass is regional. Residues are seasonal. Industrial fermentation requires continuous feedstock flow. Renewable gases and fuels must move efficiently between production, storage and end markets.

That means logistics become strategic infrastructure.

This is one of the reasons TITAN was designed around rail.

Rail is not simply a transport option.

It is one of the core foundations of industrial-scale renewable molecule production.

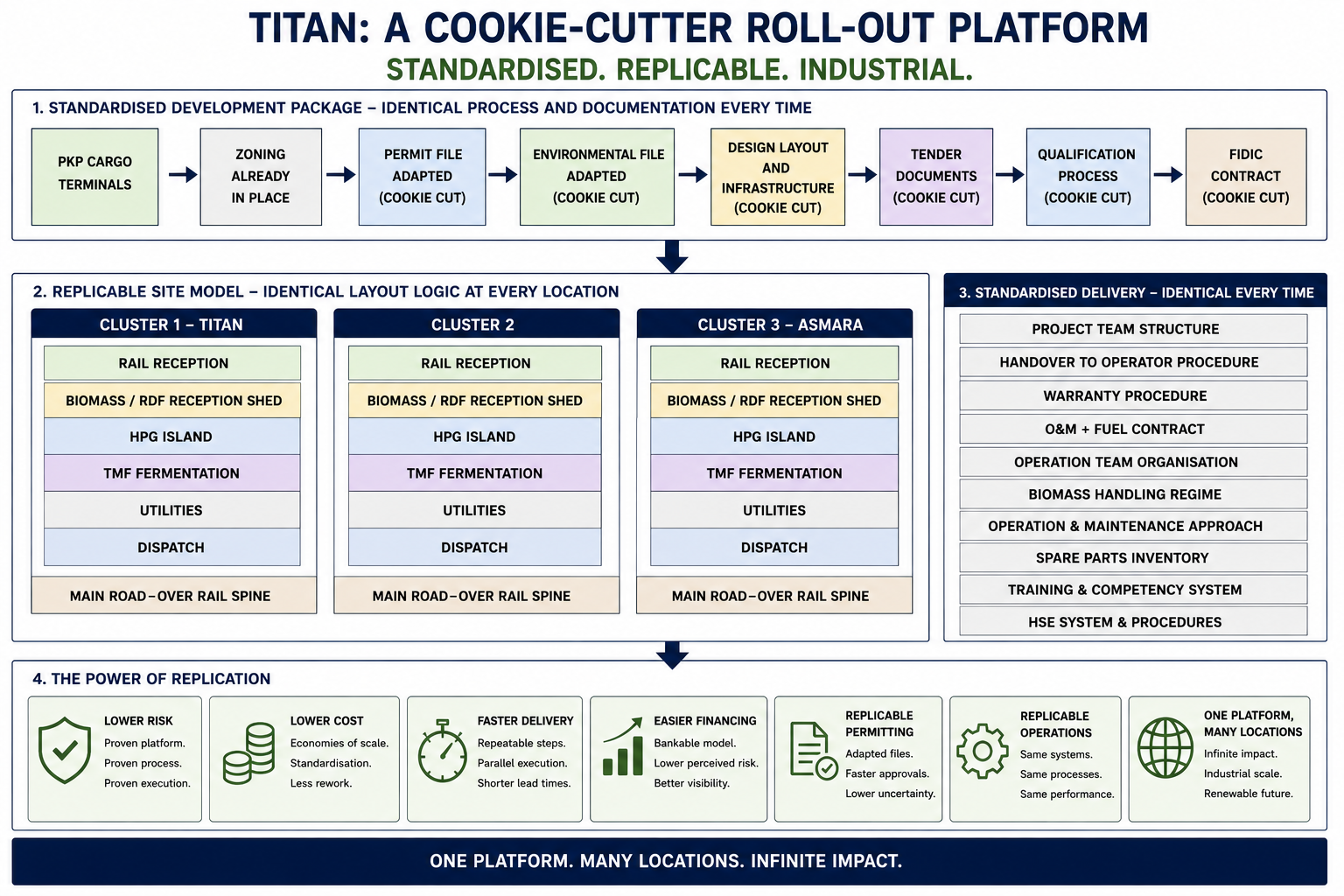

One of the biggest challenges in industrial decarbonisation is not technology.

It is replication.

Many energy and industrial projects work only under highly specific local conditions. They rely on unusual feedstocks, unique permitting structures, customised engineering or isolated infrastructure advantages. This makes scaling difficult, expensive and slow.

Europe does not only need successful demonstration projects.

Europe needs repeatable industrial platforms.

This is one of the core principles behind TITAN.

TITAN was not designed as a one-off installation.

It was designed as a cookie-cutter roll-out platform.

The objective is simple:

Standardise as much of the industrial system as possible while allowing limited adaptation to local site conditions.

This approach changes the economics and deployment logic of renewable molecule infrastructure.

In traditional industrial development, every project often starts from the beginning. Engineering teams redesign systems repeatedly. Procurement chains change. Operational training changes. Construction sequencing changes. Financing becomes more difficult because each installation appears unique.

TITAN approaches this differently.

The platform is modular, repeatable and structurally standardised.

Core systems remain consistent across deployments: gasification architecture, Hydrogen Producer Gas production, fermentation pathways, logistics logic, control philosophy and industrial workflow. This allows engineering knowledge, operational experience and supply-chain learning to accumulate over time rather than restarting for every site.

This is how industrial scaling historically succeeds.

The automotive industry did not scale through handcrafted prototypes.

Container shipping did not scale through unique containers.

Rail systems did not scale through custom track gauges for every city.

Industrial systems become powerful when they become repeatable.

TITAN applies the same principle to renewable molecule infrastructure.

Each TITAN deployment is designed around a familiar industrial structure: renewable carbon intake, gasification, controlled Hydrogen Producer Gas production, fermentation pathways, molecule upgrading, logistics integration and dispatch.

A sceptical investor may reasonably ask a simple question.

What is biochar?

Is it just charcoal?

Is it something for barbecues?

And if it can really be worth much more money, why is Syngas Project not simply making the highest-value version from day one?

These are the right questions.

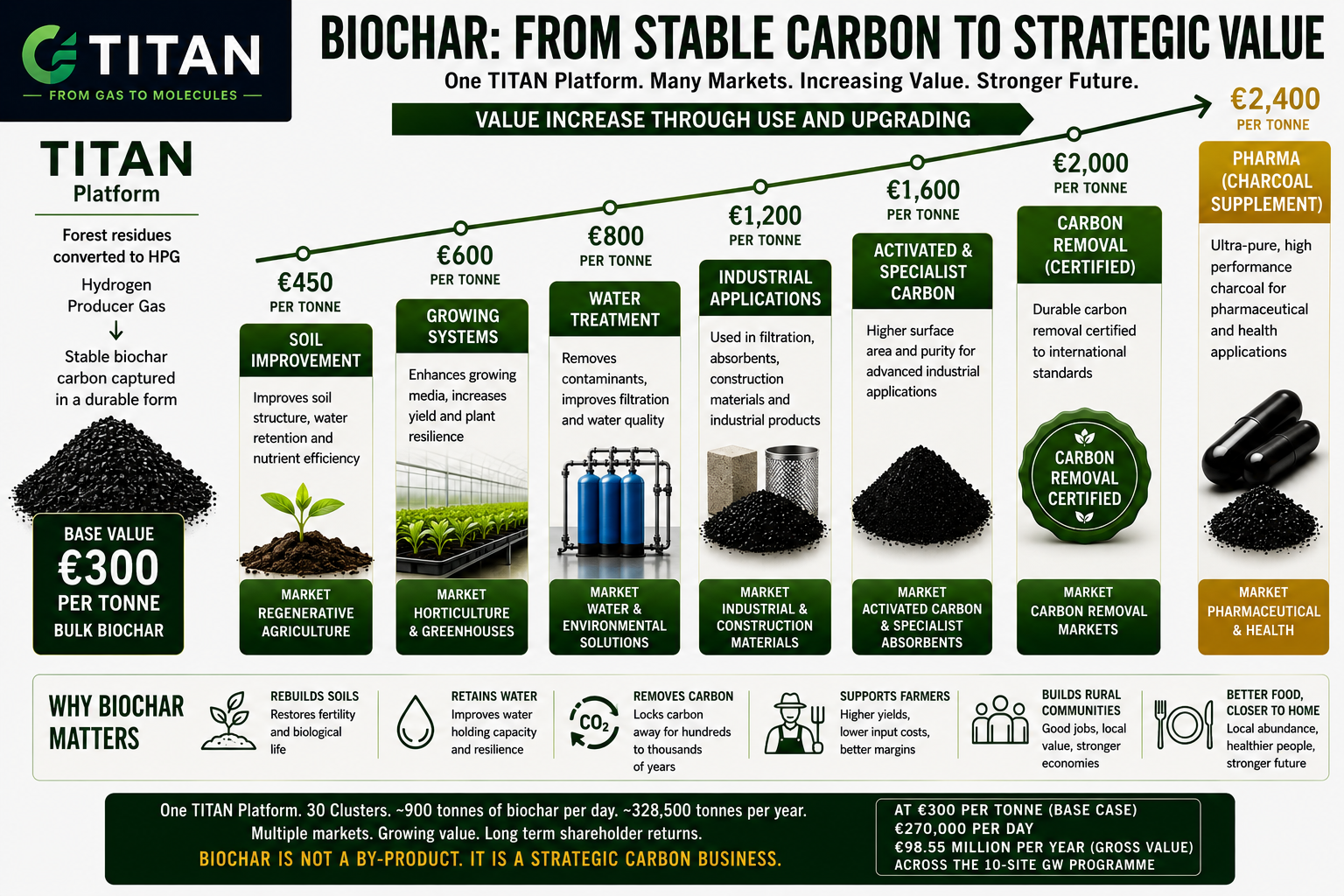

Biochar is not ordinary charcoal. Charcoal is usually made for burning. Biochar is made to remain stable, porous and useful. It is carbon designed for function, not carbon designed for fire.

That difference matters.

In the TITAN platform, biochar is produced when forest residues are converted into Hydrogen Producer Gas. Most of the carbon is converted into useful gas-phase molecules. A smaller part remains as a stable solid carbon material. This material can hold water, retain nutrients, support microbial life, improve soils and, with further processing, become a platform for higher-value carbon products.

Syngas Project does not view biochar as a waste stream.

It views biochar as a separate carbon product business.

The starting point is scale.

One TITAN cluster can produce approximately 30 tonnes of biochar per day. A fully built TITAN site with three clusters can produce approximately 90 tonnes per day. Across the planned 10-site GW programme, this becomes 30 clusters producing approximately 900 tonnes per day.

That is approximately 328,500 tonnes per year.

At a conservative base value of €300 per tonne, this is already close to €100 million per year in potential gross product value across the GW programme.

But that is only the base case.

The real strategy is not to sell all biochar as one low-margin commodity. The strategy is to segment the product stream.

The first market is practical and immediate. Biochar can be sold into soil improvement, growing systems and regenerative agriculture. This gives TITAN a clear early product route while the platform gathers operating data, product testing data and certification evidence.

The second market is certification. Once the process is stable and independently measured, selected biochar fractions can be prepared for carbon-removal certification. Certified carbon removal can command a different value from ordinary bulk biochar because the buyer is not only buying a material. The buyer is buying evidence that carbon has been removed from the active carbon cycle and stored in a durable form.

The third market is upgrading. Some biochar fractions can be further processed into higher-value carbon materials. These may include filtration media, industrial absorbents, construction materials, water treatment products, activated carbon, specialist growing media and future engineered carbon products.

This is why Syngas Project will not rush immediately into the most complex market.

A new product business must be built in stages.

First, prove consistent production. Then prove quality. Then prove application. Then certify selected streams. Then upgrade the best fractions into higher-value markets.

That is how shareholder value is protected.

The wrong strategy would be to promise pharmaceutical, battery or advanced material markets before the product specification, certification and customer base are properly established.

This is where the investor story becomes important.

Biochar may become a billion-dollar market segment because it sits at the intersection of carbon removal, soil restoration, water management, sustainable materials and regenerative farming. TITAN has the potential to produce biochar continuously, predictably and at industrial scale.

That is rare.

Small biochar producers may have a useful product. TITAN has the potential to create a platform-scale carbon materials business.

But the most important part of the story is not only financial.

Syngas Project believes regenerative farming will become one of the major economic and social shifts of the next generation.

Industrial farming has produced enormous food volumes, but often by exhausting soil, increasing chemical dependency, reducing biodiversity and making farmers work harder for lower margins. Many soils have been pushed too far. More fertiliser is not always the answer. More chemistry is not always the answer. Bigger machines are not always the answer.

The answer may be better biology.

Healthy soils can hold more water. They can support stronger microbial life. They can reduce nutrient loss. They can help growers produce better food on smaller areas of land with less stress, less waste and more resilience.

Biochar can help support that transition.

It is not magic. It is not a single solution. But it can become one of the practical tools that allows farmers and growers to rebuild soil quality, improve water retention and increase biological productivity.

This is why Syngas Project sees biochar as part of a wider abundance economy.

Abundance does not only mean producing more industrial volume. It also means producing better food, closer to people, with healthier land, better local jobs and stronger rural communities.

A future shaped by artificial intelligence and automation should not mean removing people from productive life. It should create the chance for more people to return to meaningful, skilled, local work connected to food, land, water and biological systems.

That is where regenerative farming becomes strategic.

It is not only an environmental idea.

It is a jobs idea. It is a health idea. It is a food security idea. It is a rural renewal idea. It is an abundance idea.

TITAN’s role is to provide the industrial backbone.

Forest residues become Hydrogen Producer Gas. Hydrogen Producer Gas becomes renewable molecules. Part of the carbon becomes stable biochar. That biochar can then support soils, growers, carbon removal and higher-value carbon markets.

This is not a barbecue story.

It is a carbon strategy.

And for investors, that is the point.

Biochar is not the largest product stream inside TITAN today. But it may become one of the most valuable strategic options inside the platform.

Syngas Project intends to build that value carefully, in stages, with the objective of turning stable carbon into a long-term shareholder return opportunity.

Biochar: Przekształcanie Stabilnego Węgla w Produkt Strategiczny

Sceptyczny inwestor może zadać bardzo proste pytanie.

Czym właściwie jest biochar?

Czy to po prostu węgiel drzewny?

Czy to coś do grilla?

A jeżeli naprawdę może być wart znacznie więcej, dlaczego Syngas Project nie produkuje od razu jego najdroższej wersji?

To są właściwe pytania.

Biochar nie jest zwykłym węglem drzewnym. Węgiel drzewny jest zwykle produkowany po to, aby go spalić. Biochar jest produkowany po to, aby pozostał stabilny, porowaty i użyteczny. To węgiel zaprojektowany do funkcji, a nie do ognia.

Ta różnica ma znaczenie.

W platformie TITAN biochar powstaje podczas konwersji pozostałości leśnych na Hydrogen Producer Gas. Większość węgla zostaje przekształcona w użyteczne molekuły gazowe. Mniejsza część pozostaje jako stabilny stały materiał węglowy. Materiał ten może zatrzymywać wodę, magazynować składniki odżywcze, wspierać życie mikrobiologiczne, poprawiać gleby, a po dalszym przetwarzaniu stać się podstawą produktów węglowych o wyższej wartości.

Syngas Project nie traktuje biocharu jako odpadu.

Traktuje biochar jako osobny biznes produktów węglowych.

Punktem wyjścia jest skala.

Jeden klaster TITAN może produkować około 30 ton biocharu dziennie. W pełni rozwinięta instalacja TITAN z trzema klastrami może produkować około 90 ton dziennie. W planowanym programie GW obejmującym 10 lokalizacji oznacza to 30 klastrów produkujących około 900 ton dziennie.

To około 328 500 ton rocznie.

Przy konserwatywnej wartości bazowej 300 euro za tonę daje to potencjalną wartość brutto bliską 100 milionów euro rocznie w skali programu GW.

Ale to tylko punkt wyjścia.

Prawdziwa strategia nie polega na sprzedaży całego biocharu jako jednego niskomarżowego produktu masowego. Strategia polega na segmentacji strumienia produktu.

Pierwszy rynek jest praktyczny i natychmiastowy. Biochar może być sprzedawany do poprawy gleb, systemów upraw i rolnictwa regeneracyjnego. Daje to TITAN jasną drogę do pierwszych przychodów, podczas gdy platforma gromadzi dane operacyjne, wyniki badań jakościowych i materiał do certyfikacji.

Drugi rynek to certyfikacja. Po ustabilizowaniu procesu i niezależnym potwierdzeniu danych wybrane frakcje biocharu mogą zostać przygotowane do certyfikacji usuwania CO₂. Certyfikowane usuwanie węgla może osiągać inną wartość niż zwykły biochar masowy, ponieważ nabywca kupuje nie tylko materiał. Kupuje dowód, że węgiel został usunięty z aktywnego obiegu węgla i zmagazynowany w trwałej formie.

Trzeci rynek to uszlachetnianie. Niektóre frakcje biocharu mogą być dalej przetwarzane w materiały węglowe o wyższej wartości. Mogą to być media filtracyjne, absorbenty przemysłowe, materiały budowlane, produkty do uzdatniania wody, węgiel aktywny, specjalistyczne podłoża uprawowe oraz przyszłe inżynieryjne produkty węglowe.

Dlatego Syngas Project nie będzie od razu wchodzić w najbardziej złożone rynki.

Nowy biznes produktowy trzeba budować etapami.

Najpierw trzeba udowodnić stabilną produkcję. Następnie jakość. Następnie zastosowanie. Następnie certyfikować wybrane strumienie. Następnie uszlachetnić najlepsze frakcje dla rynków o wyższej wartości.

Tak chroni się wartość dla akcjonariuszy.

Błędną strategią byłoby obiecywanie rynków farmaceutycznych, bateryjnych lub zaawansowanych materiałów zanim specyfikacja produktu, certyfikacja i baza klientów zostaną właściwie zbudowane.

Właściwa strategia to etapowe podnoszenie wartości.

Biochar masowy daje wczesne przychody. Biochar certyfikowany daje wyższą wartość. Biochar inżynieryjny daje długoterminowy potencjał wzrostu.

Tutaj zaczyna się ważna historia inwestycyjna.

Biochar może stać się miliardowym segmentem rynku, ponieważ znajduje się na styku usuwania węgla, odbudowy gleb, gospodarki wodnej, zrównoważonych materiałów i rolnictwa regeneracyjnego. TITAN ma potencjał, aby produkować biochar w sposób ciągły, przewidywalny i w skali przemysłowej.

To rzadkie.

Mali producenci biocharu mogą mieć użyteczny produkt. TITAN ma potencjał stworzenia platformowego biznesu materiałów węglowych.

Najważniejsza część tej historii nie jest jednak wyłącznie finansowa.

Syngas Project uważa, że rolnictwo regeneracyjne stanie się jedną z najważniejszych zmian gospodarczych i społecznych następnego pokolenia.

Rolnictwo przemysłowe wyprodukowało ogromne ilości żywności, ale często kosztem wyczerpania gleb, zależności od chemii, spadku bioróżnorodności i coraz większego obciążenia rolników przy niższych marżach. Wiele gleb zostało przeciążonych. Więcej nawozów nie zawsze jest odpowiedzią. Więcej chemii nie zawsze jest odpowiedzią. Większe maszyny nie zawsze są odpowiedzią.

Odpowiedzią może być lepsza biologia.

Zdrowe gleby mogą zatrzymywać więcej wody. Mogą wspierać silniejsze życie mikrobiologiczne. Mogą ograniczać utratę składników odżywczych. Mogą pomagać producentom żywności osiągać lepsze plony na mniejszej powierzchni, przy mniejszym stresie, mniejszych stratach i większej odporności.

Biochar może wspierać tę transformację.

Nie jest magią. Nie jest jedynym rozwiązaniem. Ale może stać się jednym z praktycznych narzędzi pozwalających rolnikom i producentom odbudowywać jakość gleby, poprawiać retencję wody i zwiększać produktywność biologiczną.

Dlatego Syngas Project widzi biochar jako część szerszej gospodarki obfitości.

Obfitość nie oznacza tylko większej produkcji przemysłowej. Oznacza również lepszą żywność, bliżej ludzi, zdrowszą ziemię, lepsze lokalne miejsca pracy i silniejsze społeczności wiejskie.

Przyszłość kształtowana przez sztuczną inteligencję i automatyzację nie powinna oznaczać wykluczania ludzi z produktywnego życia. Powinna stworzyć możliwość powrotu większej liczby osób do sensownej, wyspecjalizowanej, lokalnej pracy związanej z żywnością, ziemią, wodą i systemami biologicznymi.

Właśnie tutaj rolnictwo regeneracyjne staje się strategiczne.

To nie jest wyłącznie idea środowiskowa.

To idea miejsc pracy. To idea zdrowia. To idea bezpieczeństwa żywnościowego. To idea odnowy obszarów wiejskich. To idea obfitości.

Rolą TITAN jest zapewnienie przemysłowego zaplecza.

Pozostałości leśne stają się Hydrogen Producer Gas. Hydrogen Producer Gas staje się odnawialnymi molekułami. Część węgla staje się stabilnym biocharem. Ten biochar może następnie wspierać gleby, producentów żywności, usuwanie węgla oraz rynki materiałów węglowych o wyższej wartości.

To nie jest historia o grillu.

To strategia węglowa.

I dla inwestorów właśnie to jest najważniejsze.

Biochar nie jest dziś największym strumieniem produktowym w TITAN. Ale może stać się jedną z najważniejszych strategicznych opcji wartości wewnątrz platformy.

Syngas Project zamierza budować tę wartość ostrożnie, etapami, z celem przekształcenia stabilnego węgla w długoterminową szansę zwrotu dla akcjonariuszy.

A sceptical investor may reasonably ask a simple question.

What is biochar?

Is it just charcoal?

Is it something for barbecues?

And if it can really be worth much more money, why is Syngas Project not simply making the highest-value version from day one?

These are the right questions.

Biochar is not ordinary charcoal. Charcoal is usually made for burning. Biochar is made to remain stable, porous and useful. It is carbon designed for function, not carbon designed for fire.

That difference matters.

In the TITAN platform, biochar is produced when forest residues are converted into Hydrogen Producer Gas. Most of the carbon is converted into useful gas-phase molecules. A smaller part remains as a stable solid carbon material. This material can hold water, retain nutrients, support microbial life, improve soils and, with further processing, become a platform for higher-value carbon products.

Syngas Project does not view biochar as a waste stream.

It views biochar as a separate carbon product business.

The starting point is scale.

One TITAN cluster can produce approximately 30 tonnes of biochar per day. A fully built TITAN site with three clusters can produce approximately 90 tonnes per day. Across the planned 10-site GW programme, this becomes 30 clusters producing approximately 900 tonnes per day.

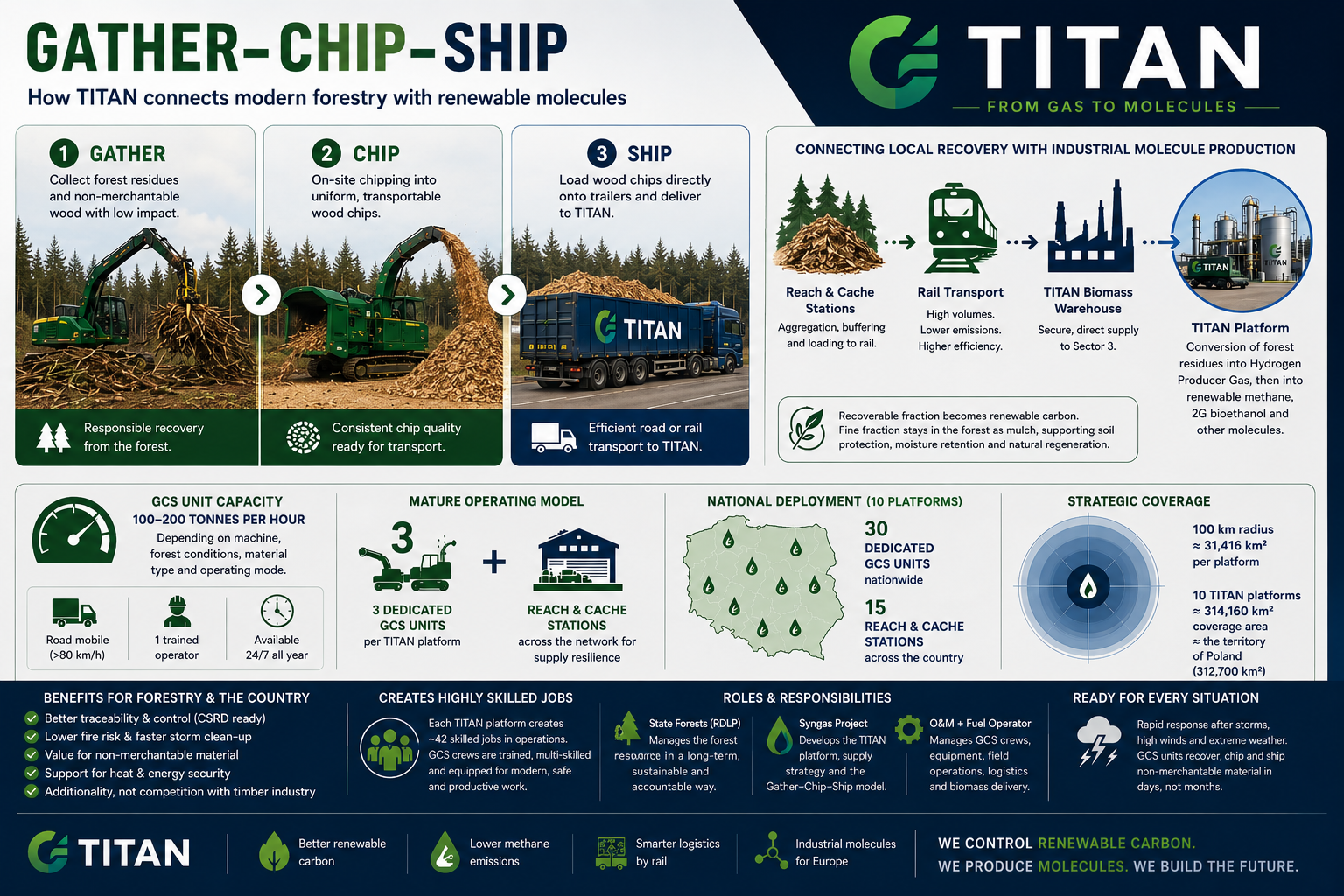

For decades, forest residue has been viewed in two simplistic ways.

Either it is treated as waste that should be removed completely from the forest floor, or it is treated as untouchable material that must remain exactly where it falls.

Reality is more nuanced.

A healthy forest is not built by abandoning unmanaged residue indefinitely. Nor is it built by stripping the forest clean. Sustainable forestry requires balance between recovery, regeneration, biodiversity, fire management, soil protection and long-term carbon stability.

This is where TITAN’s Gather–Chip–Ship (GCS) model becomes important.

GCS is not designed to “mine” the forest. It is designed to selectively recover surplus woody residues while deliberately retaining the biologically active nutrient fraction where it belongs: on the forest floor.

This distinction matters enormously.

When forest residues are chipped and processed in the field, the material naturally separates into fractions. Larger woody fractions contain most of the recoverable carbon value suitable for conversion into renewable molecules such as renewable methane, ethanol, chemicals and sustainable aviation fuel intermediates.

The finer material behaves differently.

Needles, leaves, bark particles, small twigs, dust, fragmented organics and chipped fines contain much of the rapidly recyclable nutrient content required for healthy soil ecosystems. These materials decompose quickly, retain moisture, protect the soil surface, support fungal networks and microbial life, and help feed the next forest rotation.

In practical terms, the forest floor receives a pre-mulched biological layer.

This acts almost like a natural compost blanket.

It reduces erosion. It slows water loss. It moderates temperature fluctuations at soil level. It supports mycorrhizal activity. It returns nutrients back into the biological cycle far faster than large woody residues that may otherwise remain exposed for years.

This is one of the reasons why modern sustainable forestry increasingly focuses on selective recovery rather than total extraction.

Many people imagine forest residues as a random, scattered and uncertain resource. They picture a loose biomass market, occasional availability and a feedstock supply chain that is difficult to control.

Nothing could be further from the real position in Poland.

Poland’s State Forests are one of the country’s great strategic assets. They are organised through 17 Regional Directorates of State Forests, known as RDLPs. Across more than 9 million hectares of forest, the system is planned, measured and managed over long biological cycles. Forest stands mature over 40 years and longer. Harvesting, replanting, thinning, species management and timber classification are not accidental. They are known, recorded and managed.

This matters for TITAN.

It also matters for the long-term CSRD logic of forestry.

A platform that converts forest residue into renewable molecules cannot depend on guesswork. It must understand where material is available, when it will be available, what quality it has and how much can be responsibly recovered.

The Polish forestry system already contains much of that knowledge.

The RDLP structure knows its forests. It knows stand maturity, species composition, harvest planning, merchantable timber availability and non-merchantable material potential. It understands where forest residues arise, where windthrow or disease has affected stands, and where clean-up work is required after harvesting.

This means the non-merchantable resource can be accounted for down to the tonne.

That changes its status.

Instead of being treated as a low-value residue, unmanaged by-product or potential liability, it becomes an auditable renewable carbon resource. It can be measured, recovered, priced and reported. For forestry, this is important. CSRD requires better evidence, better inventory logic and better explanation of how environmental resources and impacts are managed.

TITAN helps make that possible.

TITAN is not only a plant waiting at the end of a supply chain. It is active at the front end. The platform is designed around its own Gather–Chip–Ship capability, known as GCS. This means dedicated mobile machinery, trained operators and a controlled recovery system located around the regional forest base.